Thread Starter

#1

Hi,

A colleague of mine is looking to go for a car loan to buy a Vw vento. He's getting these types of loans-

Government banks

8.70%-8.80% rate in different banks. Sbi's rate is 8.80% File charges around 800-1000 No prepayment or preclosure charges. Interest rate is floating, might be increased or decreased as per Rbi's policy. Banks call it reducing rate though. How is it calculated BTW?

Private banks

7.70%-7.80% rate. File charges around 4500-5500 if preclosed before 25 months then 2% penalty on principal amount. Interest rate is fixed.

Private loan agencies (suggested by sales guy, probably because he's getting a share)

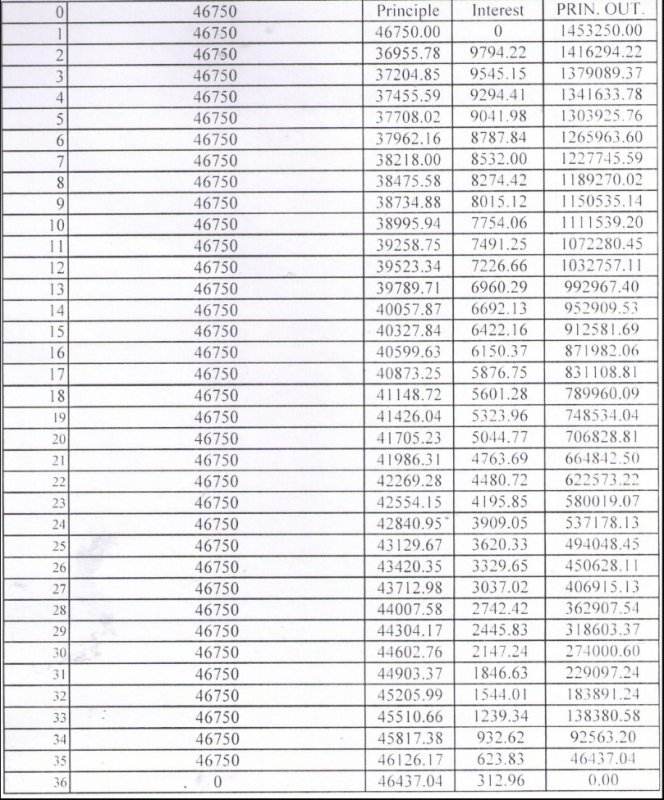

7.40% interest rate. File charges 4500-5000. If preclosed before 25 months then 2% penalty on principal amount. Interest rate is fixed. The concerned said that the auto loan will be from hdfc. But hdfc's rate is like 7.80% when asked he said we have additional powers so rate is reduced. He's not a hdfc employee but he said that all papers where we will sign will be from hdfc, he's just a middleman. He showed few loan approved papers to him according to which he got loans of 10 people approved in 2 days from the back.

VW finance

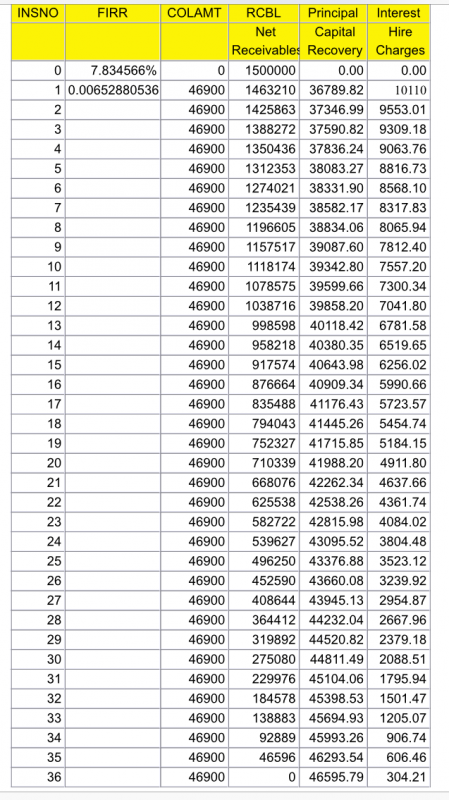

7.84% interest rate. File charges 6500. If preclosed before 25 months then 2% penalty on principal amount. Interest rate is fixed. They were the least interested people as per him.

Which loan should he select and why? Any hidden charges in private sector?

Thanks

A colleague of mine is looking to go for a car loan to buy a Vw vento. He's getting these types of loans-

Government banks

8.70%-8.80% rate in different banks. Sbi's rate is 8.80% File charges around 800-1000 No prepayment or preclosure charges. Interest rate is floating, might be increased or decreased as per Rbi's policy. Banks call it reducing rate though. How is it calculated BTW?

Private banks

7.70%-7.80% rate. File charges around 4500-5500 if preclosed before 25 months then 2% penalty on principal amount. Interest rate is fixed.

Private loan agencies (suggested by sales guy, probably because he's getting a share)

7.40% interest rate. File charges 4500-5000. If preclosed before 25 months then 2% penalty on principal amount. Interest rate is fixed. The concerned said that the auto loan will be from hdfc. But hdfc's rate is like 7.80% when asked he said we have additional powers so rate is reduced. He's not a hdfc employee but he said that all papers where we will sign will be from hdfc, he's just a middleman. He showed few loan approved papers to him according to which he got loans of 10 people approved in 2 days from the back.

VW finance

7.84% interest rate. File charges 6500. If preclosed before 25 months then 2% penalty on principal amount. Interest rate is fixed. They were the least interested people as per him.

Which loan should he select and why? Any hidden charges in private sector?

Thanks